Sustainable Procurement with Supplier Performance Management

Microsoft is taking giant leaps forward in sustainability. A new report shows the company is now requiring suppliers to report on efforts to prevent slave labor and corruption in the supply chain, and it’s working. After implementing the Tier 1 Model Factory Scorecard in 2013, which tracks suppliers’ ability to provide proper living and working conditions, Microsoft now sees every one of its Tier 1 suppliers achieving a 95 percent or higher rating.

Microsoft achieved this milestone through a supplier performance management (SPM) approach to procurement. By holding suppliers accountable for meeting sustainability standards, the company was able to make significant progress in sustainability and generate real value creation. As the SPM approach continues to grow in popularity, it is important for procurement professionals to understand what the method entails and how to leverage it to create a more sustainable supply chain.

What Is Supplier Performance Management and Why Is It Rising in Popularity?

Supplier performance management moves beyond a compliance mindset, and involves motivating suppliers to embrace corporate social responsibility (CSR) initiatives, and innovate beyond the traditional factors of cost, on-time delivery and quality to achieve sustainability objectives.

On the surface, a compliance approach may seem like less work for supply chain professionals, but it is actually often the opposite and doesn’t deliver real results. When suppliers are simply required to be compliant, procurement teams tend to evaluate the same risks and under-performing suppliers over and over again, and never deal with root causes. This turns into an endless cycle that produces very little gains for both parties and makes it difficult to measure the impact on the bottom line.

With consumers now holding their favorite brands to a higher sustainability standard and supply chain due diligence regulations—the UK Modern Slavery Act, France’s Devoir de Diligence and the United States’ new trade act—requiring companies to reevaluate how they manage every tier of their supply chains, failing to meet sustainability criteria is now a legal and reputational liability for all involved. Procurement leaders should not be satisfied with simply meeting minimum compliance requirements, but rather adopt a SPM approach that holds supply partners accountable and incentivizes them to be more sustainable, ultimately creating a holistic, long-term approach to sustainability.

JPV Logistics Management have developed Three Easy Steps program to a Successful Supplier Performance Management.

Microsoft achieved this milestone through a supplier performance management (SPM) approach to procurement. By holding suppliers accountable for meeting sustainability standards, the company was able to make significant progress in sustainability and generate real value creation. As the SPM approach continues to grow in popularity, it is important for procurement professionals to understand what the method entails and how to leverage it to create a more sustainable supply chain.

What Is Supplier Performance Management and Why Is It Rising in Popularity?

Supplier performance management moves beyond a compliance mindset, and involves motivating suppliers to embrace corporate social responsibility (CSR) initiatives, and innovate beyond the traditional factors of cost, on-time delivery and quality to achieve sustainability objectives.

On the surface, a compliance approach may seem like less work for supply chain professionals, but it is actually often the opposite and doesn’t deliver real results. When suppliers are simply required to be compliant, procurement teams tend to evaluate the same risks and under-performing suppliers over and over again, and never deal with root causes. This turns into an endless cycle that produces very little gains for both parties and makes it difficult to measure the impact on the bottom line.

With consumers now holding their favorite brands to a higher sustainability standard and supply chain due diligence regulations—the UK Modern Slavery Act, France’s Devoir de Diligence and the United States’ new trade act—requiring companies to reevaluate how they manage every tier of their supply chains, failing to meet sustainability criteria is now a legal and reputational liability for all involved. Procurement leaders should not be satisfied with simply meeting minimum compliance requirements, but rather adopt a SPM approach that holds supply partners accountable and incentivizes them to be more sustainable, ultimately creating a holistic, long-term approach to sustainability.

JPV Logistics Management have developed Three Easy Steps program to a Successful Supplier Performance Management.

Cyber Exposure Growing in Global Shipping

Despite total losses remaining stable in the shipping industry during 2015, which declined slightly to 85 - the lowest total for a decade and the second year in a row annual losses fell below 100 - there is a growing risk of cyber crime, according to the latest ‘Safety and Shipping’ review released by Allianz Global Corporate and Specialty.Cyber security risks are also growing as threats can result from improper integration and interaction of cyber systems/updates,

or attacks from external sources and are not always detected.

Allianz found that while the likelihood of a cyber event that cuts off a significant portion of trade remains low at present, cyber exposure is growing.

Technical Paper: Protecting Ships: The Threat of Hackers

The 2015 accident year represents a significant improvement on the 10-year loss average, with large shipping losses having declined by 45% over the past decade, driven by an increasingly robust safety environment and self-regulation.

However, regional disparities remain as more than a quarter of all losses in 2015 occurred in the South China, Indochina, Indonesia and Philippines maritime region, which has been the top loss hotspot for the past decade.

Cargo and fishing vessels accounted for over 60% of ships lost with cargo losses increasing for the first time in three years.

While the long-term downward trend in shipping losses is encouraging, the continuing weak global economy, depressed commodity prices and an excess of ships are pressurizing costs and raising safety concerns.

The appetite for ever-larger container ships has seen cargo-carrying capacity of the largest vessels increase by over 70% in the last 10 years, to carry 19,000+ containers.

The industry may need to prepare for a $1bn+ loss in future. There are concerns that commercial pressures in the salvage business have reduced easy access to the salvors required for recovery work on this scale.

The shipping industry has been proactively working to reduce emissions, but there have been unexpected safety implications connected with the use of ultra-low sulphur fuel.

Technological advances such as “The Internet of Things”, allied with increasing reliance on e-navigation, means insurers may have less than five years to prepare for a cyber-attack or incident materializing into a hull and machinery loss.

HOW LAST MILE DELIVERY AFFECTS THE SUPPLY CHAIN IN 2016

Published by Supply Chain Technology, on April 11, 2016

The orchestration of processes and information for the procurement of goods to the “last mile” delivery to the customer is a required competency in today’s direct to consumer marketplace. The convergence of supply chain execution systems is a goal that many enterprises have yet to achieve. While some like Amazon and Walmart are well on their way, others have yet to begin the development of their strategic roadmap.

Synchronization of information across systems provides the visibility that can help enable world class customer service. This becomes even more important in the realm of last mile fulfillment as more organizations are beginning to provide the local, rapid delivery that people are learning to expect.

If more than a Just Leave On Porch (JLOP) delivery experience is required, the essential elements for local delivery within a complete Supply Chain Execution (SCE) system should include:

APPOINTMENT SCHEDULING

Outside of common Order Management Systems (OMS) features, delivery appointment scheduling capability is essential for last mile fulfillment. The ability to schedule the order delivery at the point of sale, while considering the cost of delivery and existing delivery routes, requires orchestration with the inbound lead times and outbound route planning. Event management and alerting are also becoming more common for proactive, outbound customer communications.

DELIVERY HUB MANAGEMENT

In many instances, the starting point for the last mile is a regional facility rather than a Distribution Center (DC) or Fulfillment Center (FC). DC’s and FC’s will already have a robust Warehouse Management System (WMS). As many regional delivery hubs do not require the full breadth and depth of a WMS, some basic functionality is still needed: receiving, cross docking, inventory visibility, labor and task management, staging, driver check-in and check-out, quality audit, loading, and shipping.

ROUTE PLANNING AND OPTIMIZATION

These capabilities lie at the core of effective last mile delivery. They help drive satisfaction levels up and total cost to service the customer down. Getting more deliveries on fewer vehicles that drive fewer miles is a formula that will yield only positive results. For last mile delivery, routes can be extremely dynamic, changing day to day (sometimes intra-day) as compared with typical “service routes” that vary little from one week to the next. Best of breed capabilities are a prerequisite.

DRIVER COMPANION

Devices can vary from phones, to tablets, to “phablets”, to laptops. Basic GPS is a given, but when synchronized with the appointment management system and route optimization the driver is now fully informed and enabled. Customer information, order details, and specific delivery instructions are also provided. Proof of delivery information, including customer signature can be captured for immediate revenue recognition. Changes in customer availability can be communicated in real-time to the delivery team to reschedule and re-route.

RETURNS AND REVERSE LOGISTICS

Orders and items coming from the customer back into your supply chain is a common scenario that impacts customer service, route planning, inventory / finance, and driver awareness and cannot be overlooked when defining requirements for supply chain execution.

Throughout 2016, expect to see more SCE system providers offering greater capabilities within their applications and tighter integration with other point solutions. For last mile fulfillment, true convergence is still a work in progress. More established players will continue to close the gap while smaller, niche players will continue to require integration. A clear roadmap, with a focus on visibility across organizational silos, is needed to achieve SCE systems synchronization.

The orchestration of processes and information for the procurement of goods to the “last mile” delivery to the customer is a required competency in today’s direct to consumer marketplace. The convergence of supply chain execution systems is a goal that many enterprises have yet to achieve. While some like Amazon and Walmart are well on their way, others have yet to begin the development of their strategic roadmap.

Synchronization of information across systems provides the visibility that can help enable world class customer service. This becomes even more important in the realm of last mile fulfillment as more organizations are beginning to provide the local, rapid delivery that people are learning to expect.

If more than a Just Leave On Porch (JLOP) delivery experience is required, the essential elements for local delivery within a complete Supply Chain Execution (SCE) system should include:

APPOINTMENT SCHEDULING

Outside of common Order Management Systems (OMS) features, delivery appointment scheduling capability is essential for last mile fulfillment. The ability to schedule the order delivery at the point of sale, while considering the cost of delivery and existing delivery routes, requires orchestration with the inbound lead times and outbound route planning. Event management and alerting are also becoming more common for proactive, outbound customer communications.

DELIVERY HUB MANAGEMENT

In many instances, the starting point for the last mile is a regional facility rather than a Distribution Center (DC) or Fulfillment Center (FC). DC’s and FC’s will already have a robust Warehouse Management System (WMS). As many regional delivery hubs do not require the full breadth and depth of a WMS, some basic functionality is still needed: receiving, cross docking, inventory visibility, labor and task management, staging, driver check-in and check-out, quality audit, loading, and shipping.

ROUTE PLANNING AND OPTIMIZATION

These capabilities lie at the core of effective last mile delivery. They help drive satisfaction levels up and total cost to service the customer down. Getting more deliveries on fewer vehicles that drive fewer miles is a formula that will yield only positive results. For last mile delivery, routes can be extremely dynamic, changing day to day (sometimes intra-day) as compared with typical “service routes” that vary little from one week to the next. Best of breed capabilities are a prerequisite.

DRIVER COMPANION

Devices can vary from phones, to tablets, to “phablets”, to laptops. Basic GPS is a given, but when synchronized with the appointment management system and route optimization the driver is now fully informed and enabled. Customer information, order details, and specific delivery instructions are also provided. Proof of delivery information, including customer signature can be captured for immediate revenue recognition. Changes in customer availability can be communicated in real-time to the delivery team to reschedule and re-route.

RETURNS AND REVERSE LOGISTICS

Orders and items coming from the customer back into your supply chain is a common scenario that impacts customer service, route planning, inventory / finance, and driver awareness and cannot be overlooked when defining requirements for supply chain execution.

Throughout 2016, expect to see more SCE system providers offering greater capabilities within their applications and tighter integration with other point solutions. For last mile fulfillment, true convergence is still a work in progress. More established players will continue to close the gap while smaller, niche players will continue to require integration. A clear roadmap, with a focus on visibility across organizational silos, is needed to achieve SCE systems synchronization.

The Three States of the Global

The first step to preparing for international logistics is understanding what stage of global business your company is in currently.

Companies that simply export and import product are in the first stage of globalization. This includes companies that export products to countries where they are sold, as well as companies in the country (or elsewhere) that import everything they sell within their domestic market.

Companies in Stage Two are doing business internationally. They often work through distributors or subsidiaries, and may have some regional production and sourcing. They tend to have decentralized management and operations, as well as, a different processes and IT in place.

Companies in Stage Three are considered global, have global brands, and do business around the world. "Global companies have global sourcing and distribution, and more centralized planning,". "They think globally, operate regionally, act locally." A global company will have common processes, so that, except for local differences, a distribution center in China will operate similarly to a DC in Europe.

Operating globally creates different requirements than operating internationally. If you move to a global proposition, you have to think in terms of the entire organization, which can no longer be headquarters-driven. Instead, it should be network-driven.

Having a global mindset requires a new way of looking at how the company does business, internally as well as externally. "For example, a global company would ask, 'are our accounting, business, and sales practices prepared to take us into the areas our customers demand that we go? Do we have a diversified workforce with many cultures?'" .

These three stages can be used as starting point to develop your long term logistics strategy and milestones

Companies in Stage Two are doing business internationally. They often work through distributors or subsidiaries, and may have some regional production and sourcing. They tend to have decentralized management and operations, as well as, a different processes and IT in place.

Companies in Stage Three are considered global, have global brands, and do business around the world. "Global companies have global sourcing and distribution, and more centralized planning,". "They think globally, operate regionally, act locally." A global company will have common processes, so that, except for local differences, a distribution center in China will operate similarly to a DC in Europe.

Operating globally creates different requirements than operating internationally. If you move to a global proposition, you have to think in terms of the entire organization, which can no longer be headquarters-driven. Instead, it should be network-driven.

Having a global mindset requires a new way of looking at how the company does business, internally as well as externally. "For example, a global company would ask, 'are our accounting, business, and sales practices prepared to take us into the areas our customers demand that we go? Do we have a diversified workforce with many cultures?'" .

These three stages can be used as starting point to develop your long term logistics strategy and milestones

what is impacts or possibilities in logistics market, caused by ever increasing waste

The amount of urban waste being produced is growing faster than the rate of urbanisation, according to the World Bank’s report What a Waste: A Global Review of Solid Waste Management.

By 2025 there will be 1.4 billion more people living in cities worldwide, with each person producing an average of 1.42kg of municipal solid waste (MSW) per day – more than double the current average of 0.64kg per day.

Annual worldwide urban waste is estimated to more than triple, from 0.68 to 2.2 billion tonnes per year.

By 2025 there will be 1.4 billion more people living in cities worldwide, with each person producing an average of 1.42kg of municipal solid waste (MSW) per day – more than double the current average of 0.64kg per day.

Annual worldwide urban waste is estimated to more than triple, from 0.68 to 2.2 billion tonnes per year.

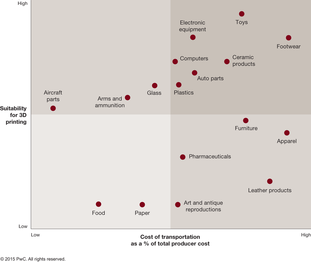

3D Printing’s Impact on the Transportation Industry

As 3D printing becomes more common, many products, their parts, or the raw materials needed in their manufacture can be made locally — reducing or eliminating the need to ship them to market. Footwear and toys, for example, are likely to require much less shipping in the future because they both have relatively higher shipping costs and are highly suitable for 3D printing.

A good example is General Electric’s jet fuel nozzles. Under the traditional method, this component contained 18 separate parts made from a variety of raw materials. All of these parts had to be machined, cast, brazed, and welded before final assembly. Now, the nozzles are made from a single alloy using 3D printers with a process known as additive manufacturing, in which successive layers of the alloy are melted, shaped, cut with lasers, cooled, and then laid down on top of each other to produce the finished part. These nozzles are lighter, more durable, and more fuel-efficient than conventionally manufactured ones, GE says.

Fully 41% of air cargo and 37% of ocean container shipments are threatened by 3D printing.

Source: Forbes

A good example is General Electric’s jet fuel nozzles. Under the traditional method, this component contained 18 separate parts made from a variety of raw materials. All of these parts had to be machined, cast, brazed, and welded before final assembly. Now, the nozzles are made from a single alloy using 3D printers with a process known as additive manufacturing, in which successive layers of the alloy are melted, shaped, cut with lasers, cooled, and then laid down on top of each other to produce the finished part. These nozzles are lighter, more durable, and more fuel-efficient than conventionally manufactured ones, GE says.

Fully 41% of air cargo and 37% of ocean container shipments are threatened by 3D printing.

Source: Forbes

Get ready for 24,000 teu, warns OECD

As the trend for ever-increasing container ship sizes continues, a new International Transport Forum (ITF)/ OECD report warns 24,000 teu vessels could be sailing the world’s oceans by 2020.

The new report, which is part of the ITF/OECD Mega-Ship project, looks at the benefits of the current mega container ships and whether they still outweigh their costs to the whole transport chain.

According to the report, 24,000 teu vessels could have major impacts on main trade lanes, would raise transport costs and could hinder the competitiveness of ports overall.

“It is likely that at some stage 24,000 teu ships will be sailing the world oceans; it is not unimaginable that this will already be the case in 2020,” says the report. “This is of course speculation; these are strategic orientations of carriers that they are not willing to share.”

The report says there are three possible scenarios: The capacity of the fully cellular fleet will grow in line with the market demand growth during the next five years, with the total fleet capacity expanding by roughly one third and containing no units of a new generation of mega carriers with capacities of up to 24,000 teu by the year 2020, or grow with 50 units of new generation carriers replacing demand for 19,000 teu vessels, or with 100 units of new generation carriers.

But, the report goes on to state that for ports in the different regions, the average ship size is only one component. “If they want to compete for the hub status, they need to be prepared to receive the largest vessels that may regularly call in the future,” it adds.

The report reveals that even if there would be no upsizing of container ships to 24,000 teu ships, the dimensions of the largest ships calling the ports in almost all regions will change, due to cascading effects. This will imply adaptations of port equipment and infrastructure in these ports to be able to handle these larger ships.

“This will be even more pressing if 24,000 teu container ships would be introduced in 2020, as this would further increase the dimensions of the ships, and thus the required infrastructure adaptations, although a more detailed study would be needed to gauge the exact extent of required changes,” the report concludes.

The report also makes recommendations to ensure countries and ports’ decisions on accommodation larger vessels aren’t detrimental. These include aligning incentives and costs to public interests – design port dues in such a way that they do not provide incentives for the largest ships – and provide policy support to ports to enhance supply chain productivity and innovation.

The report also recommends collaboration at a regional and cross-port level to help strengthen the collective bargaining position of the landside supply chain.

Source: ITF

The new report, which is part of the ITF/OECD Mega-Ship project, looks at the benefits of the current mega container ships and whether they still outweigh their costs to the whole transport chain.

According to the report, 24,000 teu vessels could have major impacts on main trade lanes, would raise transport costs and could hinder the competitiveness of ports overall.

“It is likely that at some stage 24,000 teu ships will be sailing the world oceans; it is not unimaginable that this will already be the case in 2020,” says the report. “This is of course speculation; these are strategic orientations of carriers that they are not willing to share.”

The report says there are three possible scenarios: The capacity of the fully cellular fleet will grow in line with the market demand growth during the next five years, with the total fleet capacity expanding by roughly one third and containing no units of a new generation of mega carriers with capacities of up to 24,000 teu by the year 2020, or grow with 50 units of new generation carriers replacing demand for 19,000 teu vessels, or with 100 units of new generation carriers.

But, the report goes on to state that for ports in the different regions, the average ship size is only one component. “If they want to compete for the hub status, they need to be prepared to receive the largest vessels that may regularly call in the future,” it adds.

The report reveals that even if there would be no upsizing of container ships to 24,000 teu ships, the dimensions of the largest ships calling the ports in almost all regions will change, due to cascading effects. This will imply adaptations of port equipment and infrastructure in these ports to be able to handle these larger ships.

“This will be even more pressing if 24,000 teu container ships would be introduced in 2020, as this would further increase the dimensions of the ships, and thus the required infrastructure adaptations, although a more detailed study would be needed to gauge the exact extent of required changes,” the report concludes.

The report also makes recommendations to ensure countries and ports’ decisions on accommodation larger vessels aren’t detrimental. These include aligning incentives and costs to public interests – design port dues in such a way that they do not provide incentives for the largest ships – and provide policy support to ports to enhance supply chain productivity and innovation.

The report also recommends collaboration at a regional and cross-port level to help strengthen the collective bargaining position of the landside supply chain.

Source: ITF

The digital tsunami 3.0

To set the scene for what comes next:

Clearly a vast transformation is upon us. More and more Nokias and Kodaks, unable to change, will be left behind. There will be clear winners and losers. Your company will need to disrupt or it will risk being disrupted.

In order to play this game you cannot sit still - you need the goods to implement it: a strategy, the capital and above all the institutional will. However, I'm really concerned that our large companies just aren't ready for this. Let me explain.

Situational awareness is the start

Profound change in any organisation requires both leadership and grass root buy-in.

Situational awareness is the starting point. Leadership needs to spend time in deep thought, observing and engaging with people who understand what the future holds. To do that you need to rise above the day to day noise and clutter in your business.

Above all, once you have a basic knowledge of the threat and the opportunity facing your business, you must engage with your Board of Directors to make sure they too have situational awareness and buy in to the need to act quickly.

If you don’t bring your board along, you either won’t get the budget you need to transform, or they’ll pull the rug from under your feet when you hit your first road bump. And believe me, these processes contain many road bumps.

Very few companies are even slightly prepared for the Digital Tsunami.

The trouble is, when you raise the subject of digital disruption, boards tend to look at you through glazed eyes. Your Directors were, by and large, born before Toffler’s third wave was even conceived. They just aren’t that computer-savvy and they aren’t trained to deal with these issues. They may be people of great intellect, character and expertise - but that isn’t going to be enough.

To prove the point, my colleagues and I have been researching the governance of the largest companies in Hong Kong, Singapore, Australia and New Zealand. We’ve taken the top 20 companies in each market by capitalisation, we’ve categorised them by industry and we’ve reviewed their Directors’ bios to take a guess at whether they have the right skill sets to deal with digital disruption.

To do this we’ve reviewed their LinkedIn profiles - and where Directors don’t use LinkedIn (a surprising number!) - we’ve looked at their bios from annual reports. In all we looked at 80 companies and the CVs of 800 directors. And we asked around. Lots and lots of questions.

While our process is clearly subjective and therefore open to interpretation, the results provide a sobering wake-up call:

What to do about this?

It’s the defining question for many companies today.

Each situation is clearly different. I suggest you start by raising the importance of disruption on your company's strategic agenda. Speak to your management team. Speak to your Chairman. Recruit at least one digital native onto your board. Get a digital mentor for your management and Board. Identify what the precise implications could be for your industry. Look for early signs from other markets.

Whatever you do, get it on the Board agenda, and win over your Chairman. If you don’t, your future could well look more and more like Kodak or Nokia.

Disrupt, or be disrupted.

---

Footnote: the Digital Tsunami blogs have formed the basis of keynote addresses on digital disruption at the Hong Kong Digital Entrepreneurs Leadership Forum 2015 http://delf.cyberport.hk/ and the New Zealand CEO Summithttp://www.conferenz.co.nz/conferences/nz-ceo-summit-2015 then a series of boardroom presentations around APAC. Coming to a boardroom near you!

- The first wave of disruption from 2000-2010 affected industries such as music, cameras, above-the-line media, travel and telco’s.

- Some companies think that because they survived the first wave, they are now to some extent be future-proof. Not so.

- By 2020, half the planet will be connected to the web. Four billion people will own smartphones and one billion homes will have WI-FI. There will be 50 billion connected devices and 100 million connected cars.

- The smartphone, the Internet of Things, the Sharing Economy, 3-D printing, the Cloud and Big Data will together create massive new industries - with 2020 revenues predicted to be double those of IBM, Apple, Microsoft, Samsung Electronics and Google today (I'm sure there's some double counting in there but you get the point...)

- As John Chambers from Cisco recently said, in the next decade the Internet of Things will be 5-10x more impactful than the entire Internet has been thus far.Ouch.

- Profound changes will come, with blinding speed. You will share more and more assets rather than buying them, affecting consumption. Sooner or later, you'll print things on location, disrupting manufacturing and logistics. Connected devices will provide your business with unprecedented levels of data that you'll use optimise your value chains and create unthought-of-efficiencies. Companies that don’t invest will become uncompetitive.

- 80% of today’s 100 largest companies will be outside the top 100 within 30 years. Some household names will go out of business or shrink. A legion of new companies will emerge and will make vast amounts of money as others are displaced.

- The world will be run by Gen X and Gen Y digital natives. 60% of their jobs haven’t even been invented yet. New skills will be required at all levels. Legions of people will need to retrain - like the blacksmith and the steam engineer before them, they will be ill-prepared for the future. There will be huge growth in knowledge industries. Education systems will need to change.

- Some of the current wave of disruption we’re seeing is fueled by loose monetary policy, spawning a legion of start-ups which would not necessarily see the light of day in a more conventional environment. At some point the cycle will turn and the free flow of money will stop. But for now it’s fueling the flames of disruption.

Clearly a vast transformation is upon us. More and more Nokias and Kodaks, unable to change, will be left behind. There will be clear winners and losers. Your company will need to disrupt or it will risk being disrupted.

In order to play this game you cannot sit still - you need the goods to implement it: a strategy, the capital and above all the institutional will. However, I'm really concerned that our large companies just aren't ready for this. Let me explain.

Situational awareness is the start

Profound change in any organisation requires both leadership and grass root buy-in.

Situational awareness is the starting point. Leadership needs to spend time in deep thought, observing and engaging with people who understand what the future holds. To do that you need to rise above the day to day noise and clutter in your business.

Above all, once you have a basic knowledge of the threat and the opportunity facing your business, you must engage with your Board of Directors to make sure they too have situational awareness and buy in to the need to act quickly.

If you don’t bring your board along, you either won’t get the budget you need to transform, or they’ll pull the rug from under your feet when you hit your first road bump. And believe me, these processes contain many road bumps.

Very few companies are even slightly prepared for the Digital Tsunami.

The trouble is, when you raise the subject of digital disruption, boards tend to look at you through glazed eyes. Your Directors were, by and large, born before Toffler’s third wave was even conceived. They just aren’t that computer-savvy and they aren’t trained to deal with these issues. They may be people of great intellect, character and expertise - but that isn’t going to be enough.

To prove the point, my colleagues and I have been researching the governance of the largest companies in Hong Kong, Singapore, Australia and New Zealand. We’ve taken the top 20 companies in each market by capitalisation, we’ve categorised them by industry and we’ve reviewed their Directors’ bios to take a guess at whether they have the right skill sets to deal with digital disruption.

To do this we’ve reviewed their LinkedIn profiles - and where Directors don’t use LinkedIn (a surprising number!) - we’ve looked at their bios from annual reports. In all we looked at 80 companies and the CVs of 800 directors. And we asked around. Lots and lots of questions.

While our process is clearly subjective and therefore open to interpretation, the results provide a sobering wake-up call:

- Only 10% of board members have any formal technology qualifications or, at face value, relevant business experience. I’d call very few of them digital natives.

- If you strip out telco and tech companies (because they’ve stacked their boards with tech-savvy professionals), the percentage drops to <5%.

- Very few of the directors on mainstream boards have ever experienced digital disruption first hand - on ether side of the ledger. They won’t know what to look for, and they certainly won’t know what to do when the Digital Tsunami hits them.

- This isn’t the time to be learning. To use a sports analogy, it's the time to field your strongest team. Time to get onto the field of play quickly and with winning intent.

What to do about this?

It’s the defining question for many companies today.

Each situation is clearly different. I suggest you start by raising the importance of disruption on your company's strategic agenda. Speak to your management team. Speak to your Chairman. Recruit at least one digital native onto your board. Get a digital mentor for your management and Board. Identify what the precise implications could be for your industry. Look for early signs from other markets.

Whatever you do, get it on the Board agenda, and win over your Chairman. If you don’t, your future could well look more and more like Kodak or Nokia.

Disrupt, or be disrupted.

---

Footnote: the Digital Tsunami blogs have formed the basis of keynote addresses on digital disruption at the Hong Kong Digital Entrepreneurs Leadership Forum 2015 http://delf.cyberport.hk/ and the New Zealand CEO Summithttp://www.conferenz.co.nz/conferences/nz-ceo-summit-2015 then a series of boardroom presentations around APAC. Coming to a boardroom near you!